What lies ahead for fintech and unveiling our Fintech 50 EMEA

On 23 October, we hosted more than 200 fintech founders, leaders and operators, as well as global banks and financial institutions, in London for our second Fintech Summit EMEA. You can see the full presentation here.

Since our inaugural Fintech Summit EMEA in 2022, it’s fair to say there has been a “fintech winter” casting its shadow over the industry, with funding declining and returning to the pre-covid baseline. However, this is a resilient sector that remains a significant part of the broader tech ecosystem, accounting for almost 20% of total VC funding in western markets this year. In addition, more than $250B has been deployed into fintech in western markets over the last decade, making it the first venture-fueled innovation cycle for the financial service industry.

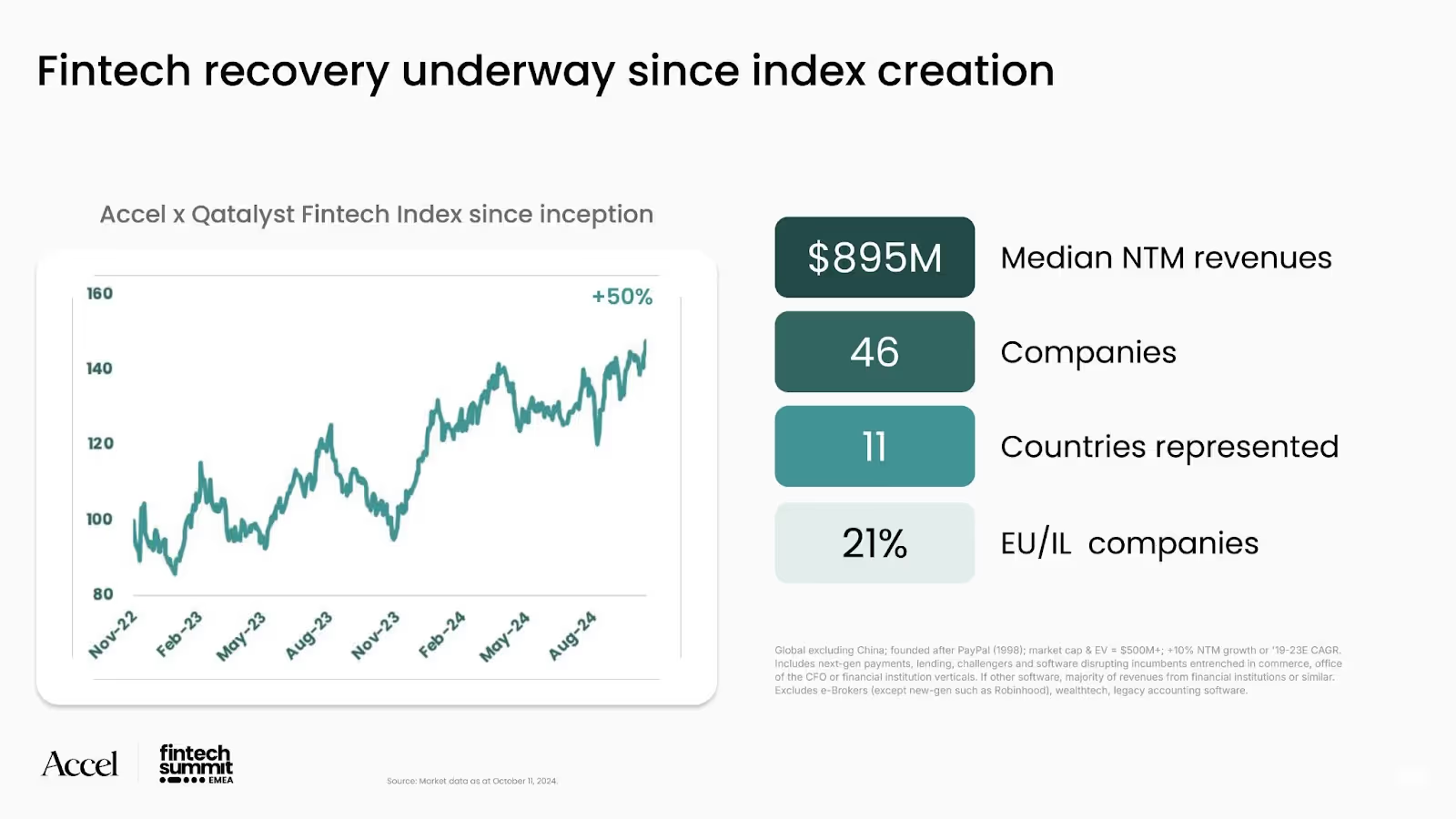

The Accel x Qatalyst Fintech Index, a global index covering world-class, growth-oriented fintechs with a combined market cap of more than $430B, also indicates that a fintech recovery is in progress. The index has increased 50% since its creation in November 2022 and performed well versus other technology sectors.

The emergence of the fintech hyperscalers

All of the money invested into fintech over the last decade resulted in a new wave of company creation, with some becoming hyperscalers.

Just a few years ago, a handful of fintech apps were appearing in our lives - limited to mostly wallets and money transfer products. Since then, there has been a tremendous innovation cycle across different categories, starting with consumer finance and payments. This wave then rapidly expanded across many other areas: insurance, lending, SME products, infrastructure, B2B use cases, and more. Many of these apps and products are now familiar elements of our everyday consumer lives and they’re becoming an increasingly common sight in our professional lives. By permeating all areas of our lives, some of the most successful fintech companies became true hyperscalers: very large, durable and enduring businesses.

All are rapidly transforming the financial services landscape, while demonstrating significant scale, growth and profitability. However, we believe we’re still very early in the journey.

The financial services industry market cap globally is more $10T and companies have only just started to disrupt the decades-old incumbents and systems that the majority of money movements happen on today. The industry is dominated by incumbents at global, regional and national levels, with significant barriers to entry that have been built and reinforced over many decades or - in some cases - centuries. In short, the opportunity is huge and there’s a well-defined market, with many clear areas to disrupt that have sizable revenue and profit pools, but it’s not an easy task and takes time.

Making the leap from private to public

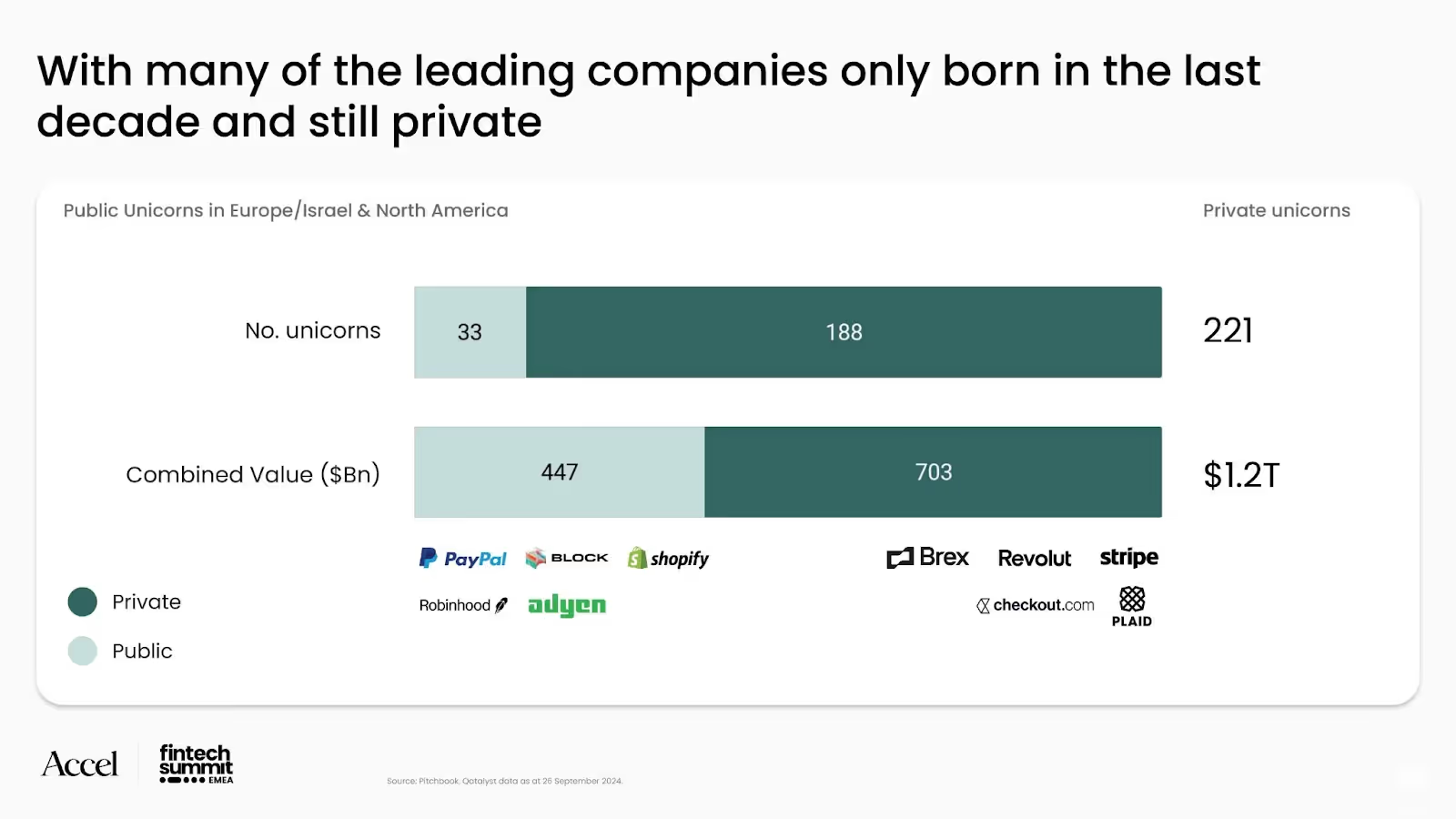

As a result of the large amounts of funding invested into fintech across all stages over the last few years, an increasing number of large private companies have emerged. There are now more than 200 public and private fintech unicorns in western markets with a combined value of approximately $1.2T, but very few have crossed the bridge into public markets. The small group of companies that have shifted across have a combined market cap of more than $400B. While a big number on its own, this is less than five percent of the broader financial services industry. Why is this the case? Put simply, it takes time to build a durable category defining business in a regulated industry and the young fintech category we’re putting under the spotlight is taking on very established, powerful incumbents.

The future: will AI usher in a new era?

The fintech industry has evolved a lot over the last two decades, often characterized by platform shifts that unlock a large amount of innovation. In the 2000s, we saw the internet shift payments online. This was then followed by the rise of mobile and cloud, and then fintech infrastructure players that powered the next generation of companies forward. Today, the hot topic is AI and - while we believe AI can be a great enabler - the question really is “how?”.

To better understand the future, we can look at how fintechs have scaled in the past and lessons learned along the way. We’ve seen fintechs make huge strides in becoming ubiquitous in the mass market - across areas such as banking and trading. Here, young fintechs that are less than 10 years old are now catching up to dominant players that have been around for decades or even hundreds of years. On the flip side, we’ve also seen incumbents hold a lot of advantage in the forms of data, distribution, and scale, and that has meant that startups have a really hard time gaining foothold, as we've seen in areas such as wealth management and insurance.

There are still key vectors that make this a good time to build fintechs.

- Finance professionals still rely on software and services dating back to a pre-cloud - ,financial services is a sector that continues to be dominated by legacy software and infrastructure that aren’t always fit for purpose. For example, Excel was invented in 1985 and, four years later, the first web server was created..

- Gen AI taking AI further in financial services - machine learning is now well established in financial services for various use cases, mainly predictive models based on traditional ML techniques used in likes of credit, fraud, transaction monitoring, customer onboarding. However, advancements in AI means more use cases can now be opened up, both in internal as well as customer facing operations. While still in the early days, we’re already seeing adoption of GenAI across code generation, product personalization, customer support, and document processing. While a lot is experimental today, we expect enduring use ceases to emerge and real ROI to be unlocked as the technology matures

- LLMs create vast opportunities for the “services” part of financial services - beyond opportunities to eat into existing software, a large part of the work and value in financial services today still lies in human work and services. The annual spend on services is staggering, and there are a wealth of inefficiencies - from accounting and advisory to outsourced processing. Repetitive processes make up the majority of costs, with a lot of hours spent doing tasks such as manual data entry, fact checking and reporting. These are use cases that LLMs can streamline with people in the loop, freeing up time and cost to be spent on higher value tasks

- Europe’s founder flywheel continues to spin - founder talent is now everywhere and, while London continues to be an incredible fintech hub, talent is also springing up from cities such as Amsterdam, Berlin, Paris, Stockholm, TelAviv, and others. There are more than 90 $1B+ fintechs across more than 20 cities in Europe and Israel - a breadth of ecosystem that you won’t find anywhere else in the world. Second generation talent is also spinning out from fintech unicorns, building not just the next generation of fintech companies, but the next generation of tech companies generally. We see this continuing to expand and accelerate over time.eeccAcccel’s Fintech 50 EMEA

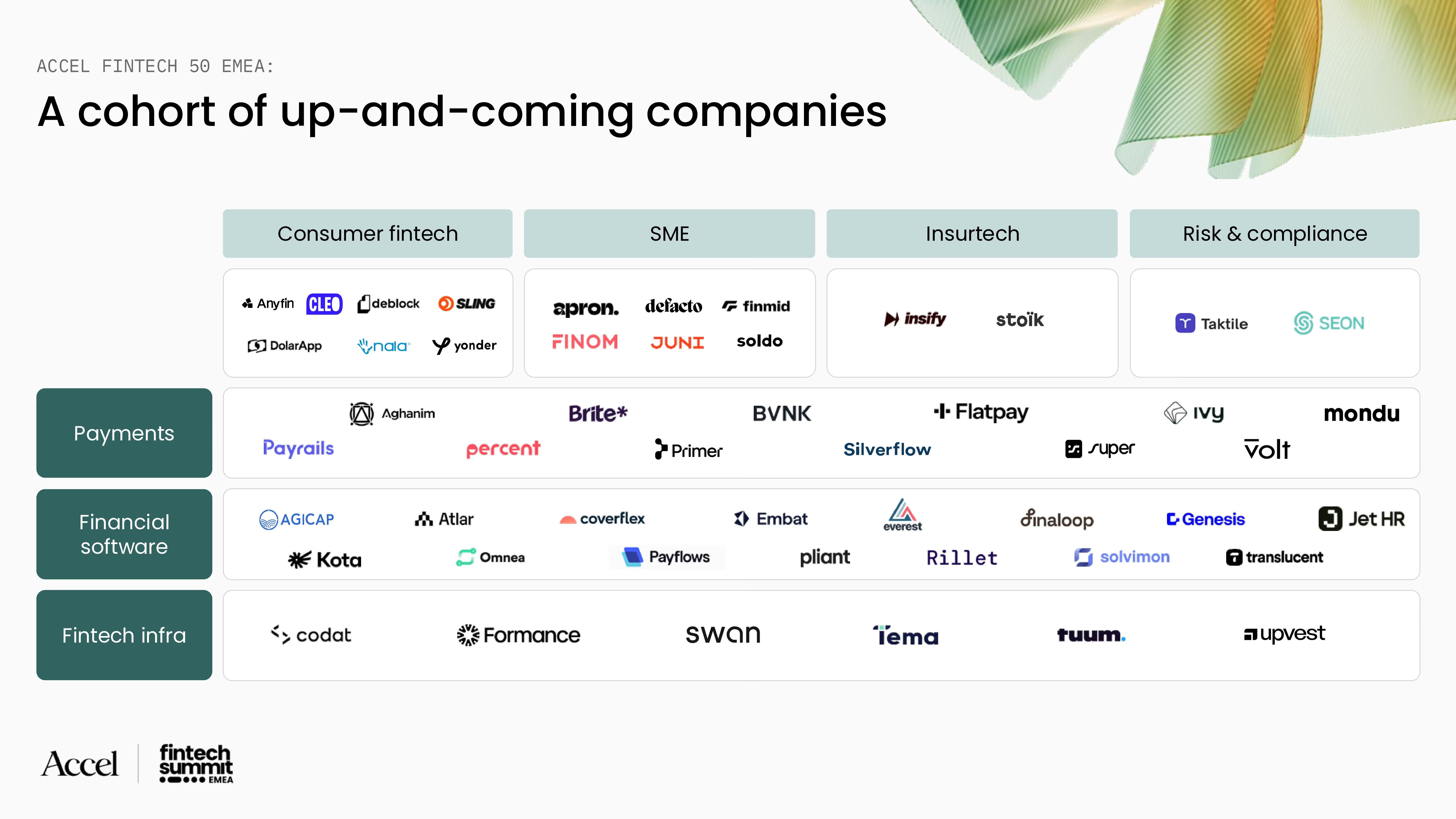

While we’ve highlighted many of Europe’s breakout fintechs, we’re also excited about what’s coming next and delighted to unveil our Fintech 50 list for EMEA. While there are more than 3,000 fintechs across 40 countries in the region, we’ve selected 50 that were founded since 2015, have raised $10M+, and are valued (for now) at less than a billion. In addition, we’ve also assessed momentum, market, product and team, to bring us to our list of 50 rising fintech stars.

There are a number of things that excite us about the 50 companies mapped out below. Firstly, a whole range of categories are represented. Secondly, we’re seeing startups from all over EMEA, with 25 cities represented. Finally, the median age of companies here is just three years old. Congratulations to all the rising fintechs that made the list!

You can see more on what the future holds for fintech here and more insight into the sessions from our Fintech Summit over the coming weeks.

Stay tuned for our predictions and the areas that we’re excited about over the coming year! You can see the full presentation here.

Great companies aren't built alone.

Subscribe for tools, learnings, and updates from the Accel community.