Prepared Mind: The European payment landscape and five predictions for the future

Our analysis on trends in payments, and where the opportunity space lies.

Our Prepared Mind series provides a snapshot of some of the areas our team has been looking at and their predictions for how the landscapes will develop (see our Insurtech article). In our next few posts, we’ll examine some of the most exciting areas in European fintech.

With money movements forming the most foundational layer for any business, naturally, we have to address the fintech behemoth that is payments.

While funding to fintech companies globally fell 18% quarter over quarter (QoQ) in Q1 2022 and the impact of turbulence in the public markets trickled down to startups, there’s still huge innovation and opportunity ahead. Q1 2022 was the best quarter ever for European fintech, up 9% from Q4 2021, and saw payments funding grow QoQ.

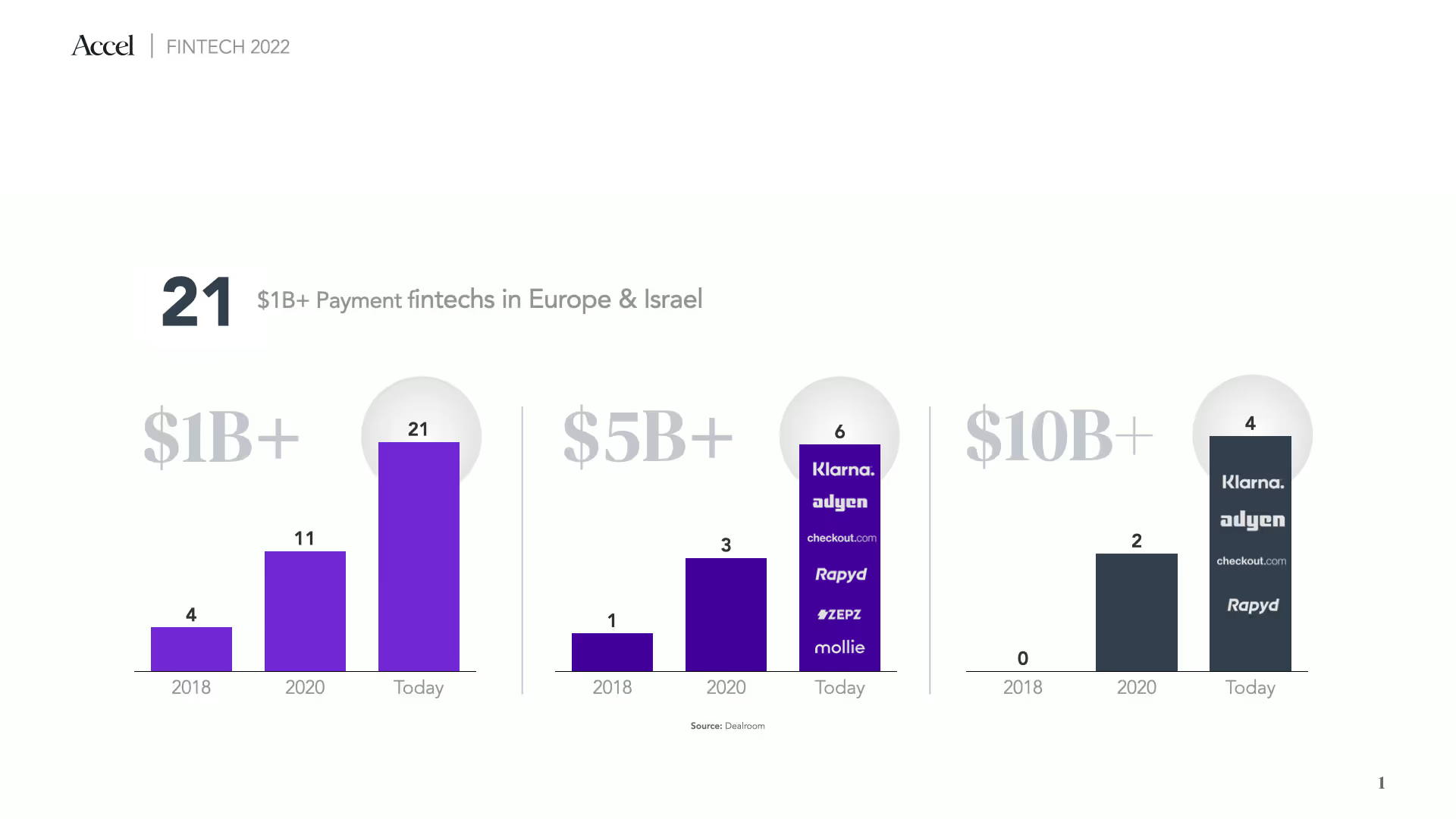

The sheer size of the global payments pie is mind-boggling, with global payments revenue totaling $1.9 trillion in 2020. While Europe and Israel have produced some of the most advanced and innovative payment tech companies to date — think Adyen, Checkout.com and Klarna — and payments is the second most invested sector in fintech as of Q2 2022 ($6.4BN of VC funding was invested in Q1 2022), we believe that we’re still only scratching the surface.

As we look at next gen payments companies and fertile ground for innovation, there are a number of areas that we feel have been overlooked and are still filled with inefficiencies that are ripe for disruption.

1. Consumerization of SME AP/AR payments and the rise of B2B BNPL

B2B payments are expected to be five times larger than B2C in terms of volume by 2028 and already account for the majority of eCommerce volume today. Yet the pace of digitization of B2B payments has lagged behind B2C, and businesses still remain vastly underserved. Buying processes are filled with friction, manual processes, long settlement periods, and high operational costs.

The total global costs related to Accounts Payable (AP) is estimated to amount to over $2.7tn3. Unsurprisingly, payments innovation on the consumer front has raised expectations when it comes to the UX of B2B payments.

We’re already partnering with early leaders that are consumerizing the B2B payments experience in order to reduce the manual friction for SMEs, such as Melio in the US.

Staggeringly, 42% of B2B payments in North America in 2019 were still carried out with paper checks, and a recent survey by Melio and YouGov found that 59% of American SMEs experience late payments.

In Europe, payments are more digitized, but B2B payments still involve more complexity than their B2C counterparts. Unlike B2C transactions, B2B transactions often involve a recurring customer base with customized needs and high order values, with a long decision-making process and multiple parties involved. Payment methods in B2B transactions commonly center around bank transfers and checks, and diverge from dominant B2C payment methods. Payment terms are also longer, and cash flow delays are frequent.

We see enormous opportunities today in solutions designed with business workflows and pain points top of mind. There’s a need for payment platforms that can seamlessly integrate with approval and accounting processes, combined with solving the most critical business need — cash flow.

B2B BNPL is an exciting area where we’ve seen more early players emerge, with a powerful proposition for multiple parties. For buyers, it can be a frictionless way to access credit to improve cash flow; for sellers, it’s a way of unlocking revenue and increasing conversion and average order values.

2. Increasing adoption of open banking as an emerging payment scheme in Europe

Despite the innovation that has occurred on the front end of payments, the rails on which consumer payments — dominated by cards — depend on haven’t changed in the last 60 years. The card networks have long had a stronghold on distribution, but PSD2 and open banking changed this, bringing in the possibility of a whole new infrastructure layer for payments to be built in Europe, with inherent distribution advantage due to the ubiquity of bank accounts.

Account to account (A2A) payments offer a powerful proposition for merchants as a cheaper, faster, more secure way of transacting. A2A payments are already common in countries like the Netherlands with iDeal and Germany with Sofort, but there has yet to be a pan-European standard. With increasing merchant awareness, maturing bank APIs, wider consumer literacy in mobile banking, as well as SCA leveling the UX between card and Open Banking payments, there is now an unprecedented backdrop for accelerating adoption of A2A payments across Europe.

Our early investment in GoCardless, and more recently in kevin. was driven by our belief that A2A and open banking represent an opportunity for payment infrastructure to be reinvented for the better.

3. Merchants to outsource more of the payments architecture and operations to third party infrastructure providers

As new payment methods emerge and gain adoption, there’s also increasing fragmentation. This creates challenges that make the reliance on a single PSP impractical (i.e. having a single point of failure, cost, lack of coverage, auth rates and conversions).

The need to manage multiple PSPs, adapt to emerging payment methods and maintain high conversion rates is creating an increasingly complex payments stack. Merchants today often have payments operations teams to handle the manual heavy lifting.

As merchants seek to reduce cost and increase flexibility, emerging third party infrastructure platforms can step in to automate many of the existing workflows. Companies like Primer enable merchants to optimize conversion rates and speed to market with a single platform and a no-code interface where users can create workflows that put the merchant’s payment infrastructure on autopilot and direct payment flows where most cost-effective.

4. Next-gen PSPs focused on servicing platforms and marketplaces to emerge

Marketplaces account for an outsized portion of consumer spending - US marketplace ecommerce sales are expected to make up 34.6% of all online sales<sup>4<sup>. The number and size of marketplaces have also been growing - 2021 marked $678 billion in marketplace exit value, with 159 new unicorns minted<sup>5<sup>.

Payments for marketplaces are notoriously complicated and difficult to manage. Onboarding and managing payments and reconciliation across multiple sellers and buyers is no easy feat. Accepting pay-ins from different buyers across different markets, grouping purchases and distributing funds to multiple sellers, managing refunds, and doing all of this in a compliant manner from a regulatory standpoint is a formidable undertaking. The likes of Zalando, Booking.com and Delivery Hero can have up to 100+ FTEs in payment operations teams.

Platforms not only have complex payments needs themselves, but also want to offer financial products to their customers, creating further layers of sub-merchant relationships and additional complexity. Shopify is a prime example as a platform that extends additional merchant services including Shopify Payments and Shopify Capital to its customers.

With the growing scale and importance of platforms and marketplaces, we believe that we will start to see more emerging players building new infrastructure to enable complex multi-relational payment flows to service platforms and marketplaces as well as their customers.

5. International payments to become faster and cheaper, and blockchain to become a new backbone for cross border payments

Cross-border payments have been increasing. SWIFT reported a 11.2% growth in traffic last year, with 2021 seeing the strongest growth in payments and securities traffic in three years. Consumer-oriented fintechs have emerged in the past few years to ease the friction and high fees related to remittance payments, but the majority of cross-border payments are B2B related, and banks still dominate 95% of the market.

SWIFT has been the juggernaut for the past 40 years, serving as the messaging network connecting the global financial network. Yet it’s filled with inefficiencies — the corresponding banking network is slow (1-5 working days), expensive (can usually cost 3-4%), and prone to human error.

When it comes to new potential solutions, we believe that new infrastructure / networks could provide a better backbone for cross border payments. We’ve seen early players that are looking to address the pain point of existing fiat rails, as well as leveraging blockchain to create new rails that bypass the need for intermediaries.

Whichever form it takes, we’re optimistic that an improved infrastructure will be in place to facilitate increasingly global payment flows cheaper, better and faster.

______________________________________________________________________________________________________________

The European payments ecosystem has yielded multiple decacorns, and is continuing to produce new waves of founders. Payments is a massive, intricate market and we’re looking forward to meeting and partnering with bold and ambitious founders who are creating the next generation of payments startups.

If you’re building the next category-defining company in the payments space, we’d love to hear from you at cwang@accel.com.

Great companies aren't built alone.

Subscribe for tools, learnings, and updates from the Accel community.